Protect your alpha

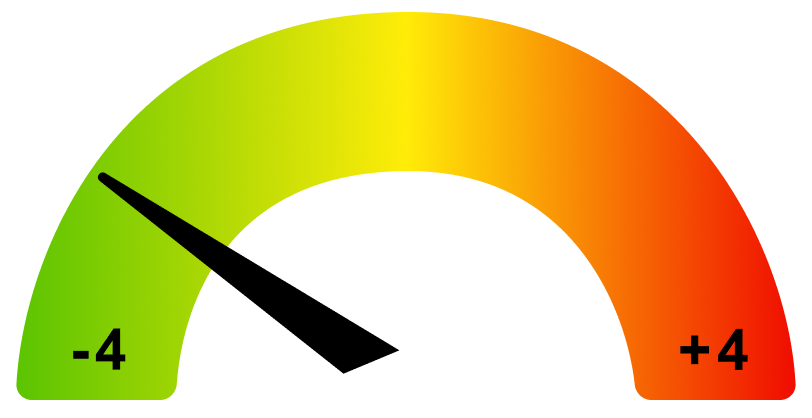

Macro Risk Pulse

The MRP is calculated using Quant Insights’ proprietary Macro Factor Equity Risk Model (MFERM)

-2.15

The Macro Risk Pulse (MRP) measures the proportion of total S&P500 risk explained by macro factors.

A high reading indicates that the market is predominantly driven by top-down macro factors opposed to company fundamental factors.

(The published figure is from the previous day closing data)

Who we help

Discover how your team can perform risk and performance analysis, find untapped alpha through unique macro data, and optimise your research process.

Multi Asset Teams

Improve execution with real-time, hassle-free notifications that help you buy and sell at the right price by leveraging precise valuation benchmarks across multiple asset classes.

Equity Portfolio Teams

Decompose individual stock returns into macro factors. Reveal true portfolio exposure and protect your alpha

We manage the macro. You focus on the alpha

Our Solutions

Strengthen your investment process with data driven repeatable and consistent macro perspectives in your portfolio. Easy to interpret and deploy.

A robust cross-asset, valuation engine to identify dislocations, between macro information and price.

Our Risk Models and Analytics help investors understand and measure how macro factors impact their portfolio risk and return.

Our Partners