Validated on 15 years of daily data. Thousands of stocks. Trusted by institutions demanding precision.

MFERM protects you from macro-driven losses and adds alpha to give you a macro edge.

Loss Protection: Reducing Key Risks

Unintended Exposure Risk

Unintended exposures bleed alpha. Quietly. Persistently. Macro crowding makes it worse—one regime shift triggers mass de-risking.

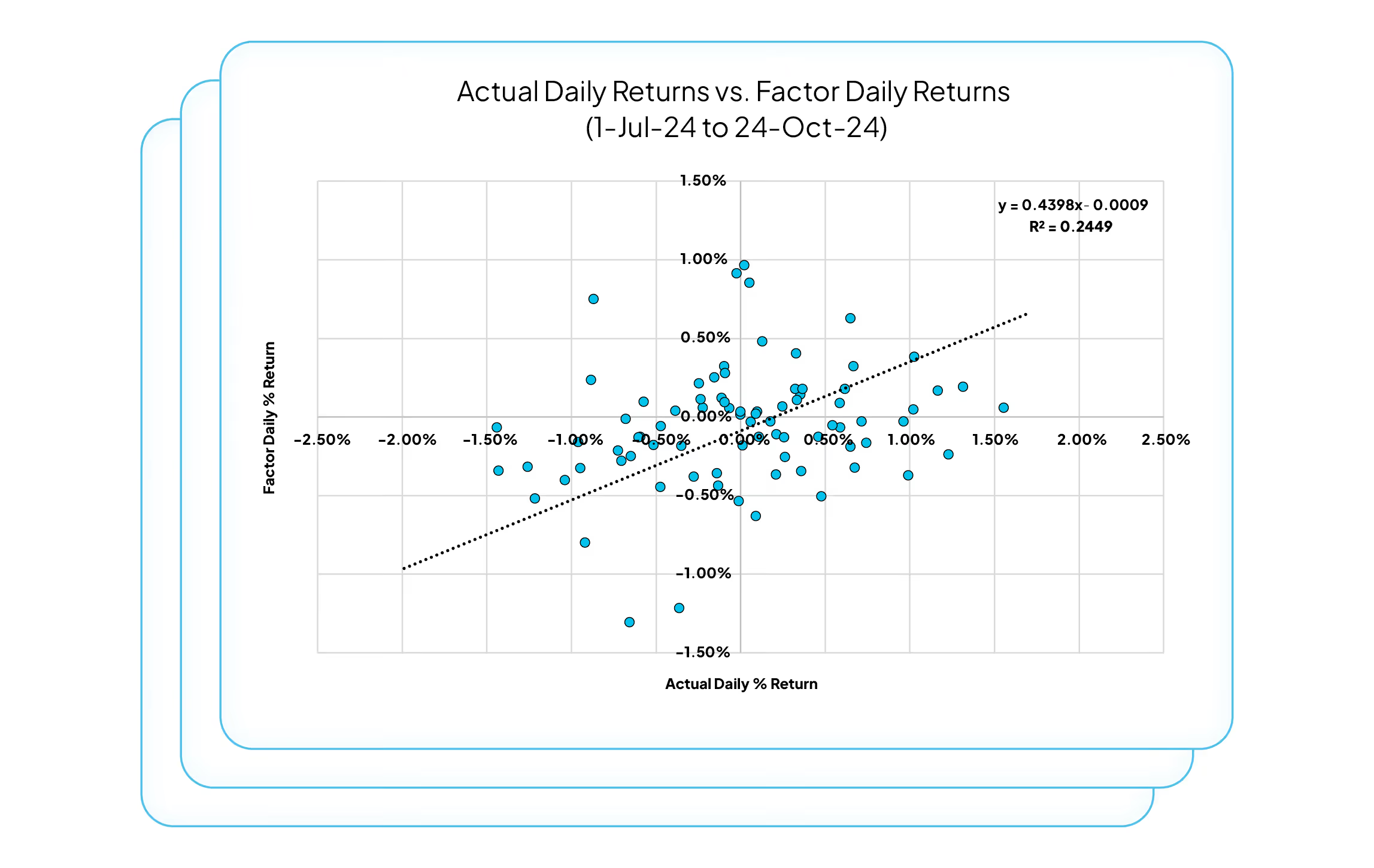

MFERM shows you both risks in real-time. Measure, monitor, and manage exposures without changing a single name. Run macro stress tests. Quantify tail risk. Reduce net portfolio exposure with precision.

Add Alpha With a Repeatable Macro Edge

• Harvest the Dual Risk Premia - Tilt toward whichever engine is paying: Macro or Idio. Proven to add +2.5% annual alpha.*

• Sharpen Stock Conviction - Use macro regime data to size positions with confidence and reduce alpha slippage.

• Transform Risk Management into Alpha - Use forward-looking Macro Share of Risk (MSR) as a signal to play defense or offense.

• Validate Strategy Integrity - Prove your fund's returns are generated by its stated process. Secure allocations.

Benefits

Accurate Macro Exposures

Stock-level exposure sensitivities derived from a model that orthogonalizes macro factors to remove multicollinearity.

Easy to Interpret

Unlike statistical models, MFERM shows exposures to macro factors themselves. Relate your risks directly to market developments.

Comprehensive Factor Set

Includes daily real GDP estimates and inflation expectations.

Multiple Model Variants

Regional models, with and without market factor, covering a broad stock universe.

Related Insights

.jpg)