Buy the Dip? Fade the Rip

What Qi's Risk Model Says Now

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

Key Takeaways:

Qi’s Risk Model forecast of S&P500 Risk is rising from multi-year lows. This is likely still in its infancy: Risk-adjusted returns from these levels tend to be weak. The structural top-down / bottom-up headwinds are not disappearing soon.

However, the jolt higher in the VIX relative to Qi’s Risk Model forecast is now at the upper-end of its recent range: History suggests that when this relative gauge has swung too far, it portends temporary respite for risky assets.

But fade the rips: With 2yrs until the mid-terms, the market problem with Trumponomics is that all the bad news likely comes first – the ramifications of DOGE cuts, tighter immigration, tariff uncertainty before the good news of tax cuts, deregulation etc. later.

The Bigger Picture:

Markets are digesting a potential US growth slowdown, with concerns the direction of travel of the US policy mix is contra to the interest of growth and earnings.

Since last summer, Qi’s Risk Model has been showing rising positive S&P500 sensitivity to the Dollar and 10yr yields. In other words, stocks up, dollar up, rates up reflects confidence in Trump’s policy agenda and the US Exceptionalism narrative. While the reverse reflects the opposite. See the charts below.

Indeed, if Europe is no longer funding the US fiscal expansion (instead they are funding their own); tariff policy slows US growth; the Fed is forced to cut rates or the Fed’s hands are tied because inflation remains sticky – it puts into question the dollar safe haven role.

Alongside the top-down uncertainty damaging consumer and business confidence, is the bottom-up uncertainty on what multiple to place on US Tech. If macro continues to dominate, the pressure on Mag7 multiples will remain high. See the chart below. This tricky mix of both top-down and bottom-up concerns will not disappear easily.

Qi Risk Model: Why it Matters

Qi’s Risk Model provides a prediction on risk. Unlike the VIX, which reacts to market swings, Qi’s model integrates asset factor exposures and their interactions. This risk forecast is a function of the asset’s factor exposures and covariance matrix of the factor returns themselves. In other words, to estimate risk, we must consider not only the asset’s exposures to the factors, but also the interaction between factors.

Factor exposures are derived from the PLS time series regression of the factors and the asset using a 1yr lookback. While the factor covariance matrix uses a 125d lookback but exponentially weighted (using a 90d half-life).

Qi’s Risk Forecast has been rising since the second half of February. Indeed, it is rising from its lowest levels post Covid, previously hit last July ahead of an 8% fall in the S&P500. This is not a level from which risk-adjusted returns will flourish. As outlined above, this tricky mix of top-down and bottom-up headwinds are not going to go away easily. In part, this is why we say fade the rips. See the charts below. The 50d Model Risk z-score has been rising but has still ample room to move higher

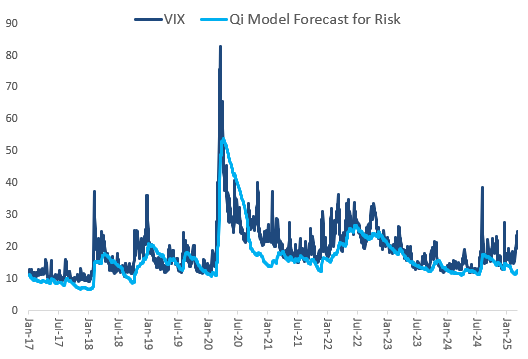

Benchmarking to the VIX Spike suggests Temporary Respite:

But we have to remain open-minded, in what is a trader’s market:

The result of our approach is a more stable forecast of risk compared to a gauge such as the VIX. The VIX, which is measuring the expected 30d vol of the S&P500 based on the price of its options, will be much more noisy. See the chart below comparing the two.

By looking at the difference between these 2 measures of risk, we can benchmark how far sentiment pendulum has swung – the relative spike in VIX is at the upper end of its range since 2021. Prior spikes to this level have portended some respite for risky asset

Disclaimer

This document is being sent only to investment professionals (as that term is defined in article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) OrdeRSq005 (“FPO”)) or to persons to whom it would otherwise be lawful to distribute it. Accordingly, persons who do not have professional experience in matters relating to investments should not rely on this document. The information contained herein is for general guidance and information only and is subject to amendment or correction. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This document is provided for information purposes only, is intended for your use only, and does not constitute an invitation or offer to subscribe for or purchase any securities, any product or any service and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document does not constitute any recommendation regarding any securities, futures, derivatives or other investment products. The information contained herein is provided for informational and discussion purposes only and is not and, may not be relied on in any manner as accounting, legal, tax, investment, regulatory or other advice.

Information and opinions presented in this document have been obtained or derived from sources believed to be reliable, but Quant Insight Limited (Qi) makes no representation as to their accuracy or completeness or reliability and expressly disclaims any liability, including incidental or consequential damages arising from errors in this publication. No reliance may be placed for any purpose on the information and opinions contained in this document. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Qi, its employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. Any data provided in this document indicating past performance is not a reliable indicator of future returns/performance. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance.

This presentation is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person under any circumstances without the express permission of Quant Insight Limited.