Navigating the Pullback:

Macro Impact on Styles

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

Key Takeaways:

Positioning a key discriminator: In the most recent pullback, non-macro drivers i.e. idiosyncratic drivers have been a key differentiating drag for High Beta and Momentum. This reflects the positioning flush. Value and Quality have held up better, where the idio component of returns has actually been positive.

Macro Drags overwhelm the Propellers: Wider credit spreads, a flatter money market strip, lower real yields and lower GDP growth have been the dominant drags. These drags overwhelmed the propellers which were higher metals, lower inflation expectations and a steeper 5s30s curve.

Value has the lowest beta to the Market across the styles shown: The brunt of the market beta rests with the Growth style.

The continued rotation to Value requires a Goldilocks regime: GDP holding up, a steeper 5s30s curve, a positive bias to higher inflation expectations but also lower real rates.

A return to Growth requires greater belief in US Exceptionalism: Real rates up, a steeper money market strip, a steep 5s30s curve and a stronger dollar bias. Growth’s beta to the market is high.

We review Value (VTV), Growth (VUG), Momentum (VFMO), Quality (VFQY) and High Beta (SPHB) ETFs through the lens of Qi’s Risk Model.

- How has Macro Moved Since the S&P 500 Peak on 19th Feb?

Across the 12 macro factors in Qi’s Risk Model, on a vol-adjusted basis:

Financial Conditions – some factors up / some down: HY corporate credit spreads have widened and rate vol has risen (CB QT expectations); in contrast, rates and the Dollar have fallen

Growth Expectations – some factors up / some down: GDP Nowcast, WTI (energy) and inflation expectations are lower; in contrast, the 5s30s curve (forward growth expectations) is steeper and copper (metals) is holding up

The relative magnitude of the moves is shown below (period change relative to daily 1SD change) e.g. the a daily 1SD move in HY credit spreads is 5.5bps. Therefore the rise of ~45bps is an 8 sigma move on this apples-to-apples measure.

Which Macro Factors Matter Most to each Style?

We ran the cited ETFs on Qi’s US Risk Model including the market i.e. to ascertain exposures taking into account market beta.

Financial Conditions Exposures:

- Credit Spreads: High Beta and Momentum have the largest negative sensitivity to wider HY credit spreads.

- CB Rate Expectations: With the exception of Value, styles want a steeper money market strip – reflecting a desire for near term rate cuts that fuel better economic growth looking forward. But recession talk has seen the strip bull flatten, i.e. styles - in particular High Beta wants higher 1y1y yields as a measure of confidence & fears of a hard economic landing hurt.

- Real Rates: High Beta, Momentum and Growth all want higher real rates; in contrast, Value is more sensitive to the cost of capital and wants to see lower real rates

- Dollar: Growth would prefer to see a higher dollar most across the styles. Most styles are largely indifferent to the Dollar right now. Fixed Income is the bigger transmission channel than FX currently

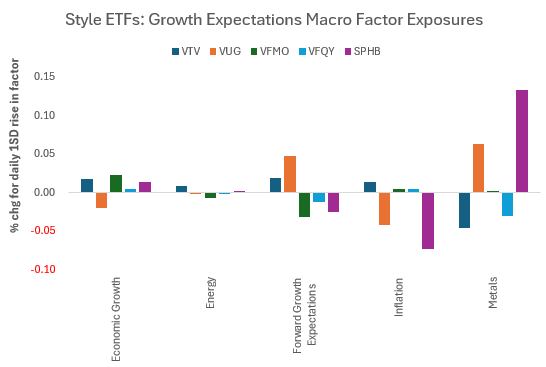

Growth Expectation Exposures:

- GDP Growth: With exception of Growth, all styles want to see higher GDP growth. There is less of a need to hunt for secular growth if there is economic growth.

- Metals: High Beta and Growth also want to see higher copper prices. Value and Quality have negative sensitivity.

- Inflation Expectations: Higher Beta and Growth would welcome lower inflation expectations the most; Value the least.

More broadly, Value wants to see higher GDP growth, higher energy, a steeper 5s30s curve, alongside higher inflation expectations i.e. a reflationary economy.

Given the Factor Moves and Different Factor Exposures, what does the Style Return Attribution show?

Non-Macro Factors (Stock-Specific Returns): Helped value and quality but hurt high beta, momentum, and growth—suggesting position unwinds in riskier styles.

Market Beta: Value has the lowest beta to the Market across the styles show – the brunt of the market beta rests with Growth.

Macro Propellers: Lower inflation expectations, higher metals, a steeper 5s30s curve and lower nominal 10yr yields have been factor return additive across most styles over this period.

Macro Drags: However, the flatter money market strip, lower real yields and wider credit spreads and higher risk aversion have more than offset.

Value’s Resilience: Notably, Value has been most insulated from the above cited drags given it sees a lower 1y1y and lower real yields as net positives.

Investors can’t control macro moves, but they can adjust exposures. This analysis highlights which styles are most vulnerable or resilient in different macro regimes—insights that can sharpen risk management and tactical positioning.

Disclaimer

This document is being sent only to investment professionals (as that term is defined in article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) OrdeRSq005 (“FPO”)) or to persons to whom it would otherwise be lawful to distribute it. Accordingly, persons who do not have professional experience in matters relating to investments should not rely on this document. The information contained herein is for general guidance and information only and is subject to amendment or correction. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This document is provided for information purposes only, is intended for your use only, and does not constitute an invitation or offer to subscribe for or purchase any securities, any product or any service and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document does not constitute any recommendation regarding any securities, futures, derivatives or other investment products. The information contained herein is provided for informational and discussion purposes only and is not and, may not be relied on in any manner as accounting, legal, tax, investment, regulatory or other advice.

Information and opinions presented in this document have been obtained or derived from sources believed to be reliable, but Quant Insight Limited (Qi) makes no representation as to their accuracy or completeness or reliability and expressly disclaims any liability, including incidental or consequential damages arising from errors in this publication. No reliance may be placed for any purpose on the information and opinions contained in this document. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Qi, its employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. Any data provided in this document indicating past performance is not a reliable indicator of future returns/performance. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance.

This presentation is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person under any circumstances without the express permission of Quant Insight Limited.