Qi Macro Spotlight - The Inflation Narrative is Shifting

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

Summary:

US inflation expectations are becoming problematic. 5 year inflation expectations arenow closer to 3% than 2% with several prominent commentators in recent weeks seeingthe risks as skewed to the upside. Two key points revealed by Qi's Macro Factor EquityRisk Model:1/ If you believe this narrative persists, the Consumer Discretionary sector is mostvulnerable-more than half of the sector has seen an increasing drag from higher inflationexpectations YTD.2/ If you believe this narrative persists, macro volatility for this sector is set to rise.Unnervingly, the factor vol as predicted by Qi's Risk Model is still sitting at the lows of thelast summer.Several studies come to the same conclusion - after staggering wealth gains, atariffbased regime for increasing tax revenues and rebalancing trade will likely come ata significant economic cost for the average household.https://budgetlab.yale.edu/research/fiscal-economic-and-distributionaleffectsillustrative-reciprocal-us-tariffs

Details:

The St Louis Fed President Alberto Musalem warned last week that "risks of inflationstalling above 2% or moving higher seem skewed to the upside."

There is greater reception now of the possibility that inflation drifts higher over thebalance of 2025 - fiscal policy / tariffs, tight labor and housing markets, robust creditgrowth etc.At the heart of Qi's Macro Factor Equity Risk Model is our time series, machine learningalgorithm to determine an asset's factor exposures. We first ran this across the S&P500universe:Where is the greatest vulnerability? The impact of higher inflation expectations on themarket will be dependent on market focus - alongside higher growth, it will be deemedreflationary. Alongside weaker growth, it will be deemed stagflationary. On anequalweighted basis, overall exposure is still bifurcated. However, there is one sectorwhich stands out for its vulnerability - Consumer DiscretionarySpecifically, in the table below, we used Qi's Risk model to identify by sector, what % ofstocks see higher inflation as a drag today AND where that drag has been becominglarger YTD (given the moves in inflation expectations).

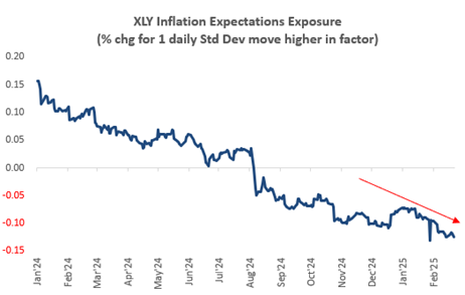

Over half the Consumer Discretionary sector see high inflation expectations as aproblem and becoming a bigger problem YTD. At the other end of the spectrum isUtilities and Energy.Indeed, the below chart shows inflation expectations exposure for XLY turn increasinglynegative since last summer:

If we plot the price relative of the book-ends i.e. XLY / XLE vs. 5yr inflation expectations we can see the empirical fit , but also note that XLY has enjoyed relative outperformancein the post-election honeymoon period.

Below we show 15 stocks from the GICs level 1 Consumer Discretionary sector within thatsubset as defined above, where the drag has been the largest YTD.We note that Walmart had earnings last week where they gave weaker than expectedguidance. Walmart had the view that if tariffs were implemented they can make theirsuppliers take the hit. However, we doubt the rest of the consumer sector has the samebargaining power. The Yale Budget Lab shows that a “reciprocal” tariff policy where the US matched othercounties’ tariff and VAT rates could increase total tax revenue in the ten years to 2035by $2.7 to $3.5 trillion -but at a significant economic cost. The price level would rise by1.7-2.1% soon after the tariffs are imposed, costing an average household between$2,700 and $3,400 while hitting the disposable income share of lower incomehouseholds the hardest.

Qi's Risk Model also predicts macro factor volatility - a function of an asset's factor exposures and the covariance matrix of the macro factors themselves. We ran this forXLY and it is unnerving to see predicted factor vol for XLY back at last year's lows - thatwas last summer when the sector saw a >10% correction. This is not to mean we will seethe same, but the simple point that low predicted factor vol is a sign of complacency ifyou believe macro is in play.