1. SPY - Amber warning from macro uncertainty

2. Pole Position Pricing

3. US - Europe

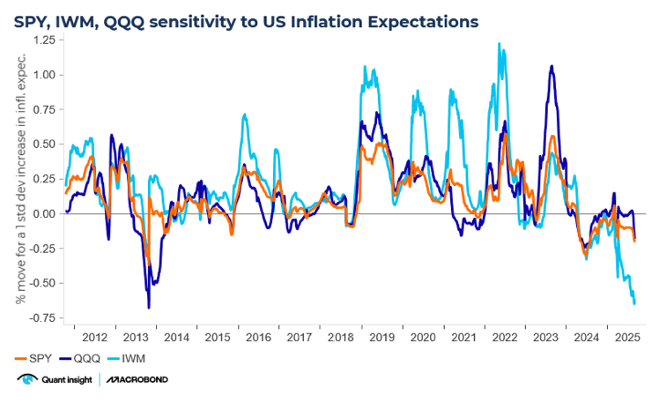

1. Small Cap rotation is hostageto inflation

2. Rate Volatility - the BlindSpot in Equity Risk

3. Rising Rate Vol - the AchillesHeel of IBB

1. SPY - amber warning from macro uncertainty

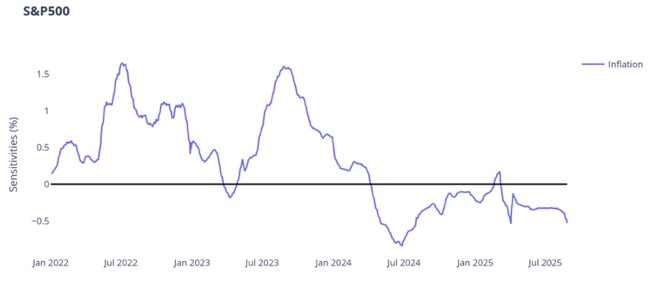

Qi model confidence for the S&P500 is close to multi-year lows. Right now, macro canonly explain 27% of the variance of the SPY ETF.

This is an unnerving sign –the market is struggling to interpret the US equity narrative. Thisis not surprising given the question marks on US exceptionalism.Early in 2025 we're seeing economic surprises / Atlanta Fed GDP nowcast fading at thesame as several Fed speakers warn of upside risks to inflation - the growth / inflationtango is turning anti-Goldilocks. This, coupled with high policy uncertainty, is keepingthe distribution of outcomes wide.As the narrative becomes clearer, Qi model RSq will rise; but history suggests at thesepoints caution is warranted. This adds to the warnings signs we have been citing from Qi’sRisk Model.

2. Pole Position Pricing

The Polish WIG20 is up 19% YtD reflecting increasing confidence that war in Ukraine isending & the re-build process can begin.The iShares ETF tracking MSCI Poland now sits 2.2 sigma (10.93%) rich to macrowarranted fair value, the biggest Fair Value Gap in Qi's model history.Clearly the end of armed conflict represents a huge positive exogenous shock. Still,theimplication is a lot of Ukraine optimism is now in the price of Polish equities.

This is also notable given the role Polish equities have played as a barometer ofconfidence in the rally in Europe more broadly. Put another way, it could be seen as awarning a peace dividend is increasingly discounted in pan-European stocks.

3. US - Europe

Last week's MacroVantage observed that 10y Bund yields sat 1.1 sigma too high relativeto prevailing macro conditions. They've fallen 10bp since then & Qi's FVG has halved.The bigger dislocation now is less on outright levels, more on relative performance. OnQi, the 10y UST-Bund spread is 0.9 sigma (20bp) too tight, 30y UST-Buxl spreads are 1sigma (19bp) too tight.US yields have moved lower relative to German yields as markets focus on the downsiderisks to US economic growth but upside risks to Bund issuance.

The issue is while macro momentum does point to spread tightening, model value has yetto fall below 200bp, i.e. the market has moved ahead of macro fundamentals. And, givenrecent correlation patterns, the FVG could flag this move is starting to look extended.

.png)