1. The Trump Discount - EURUSD

2. SPY sensitivity to Dollar& 5s30s hitting extremes

3. What's priced? Global government

1. The Trump Discount - EURUSD

The fx market is debating whether capital flows now dominate interest ratedifferentials and therefore justify a structurally lower Dollar.

There several good reasons to think we're only just starting to see a secular shift -a reallocation away from US to European/Asian assets. Does that explain why EURUSD remains elevated despite this week's narrowing in USD-EUR cross-market yieldspreads?

Official capital flow data is low frequency, lagged and noisy. So Qi employs a proxy factor to capture this narrative. A steeper US yield curve reflects the additional risk premium in US assets - the chaos premium for Trump policy uncertainty.

Negative sensitivity means a flatter EUR yield curve relative to the US is consistentwith higher EURUSD. And sensitivity to this factor is at multi-year extremes.

TheQi framework offers a multi-dimensional approach. Right now taking account interest rate differentials, relative curve shape and multiple other macro factors, macro-warranted fair value is 1.09. The spot market trades 4 big figures north of there, which is a +1.6 std dev Fair Value Gap.

Even with secular tailwinds, the risk-reward suggests these aren’t great levels to chase EURUSD upside.

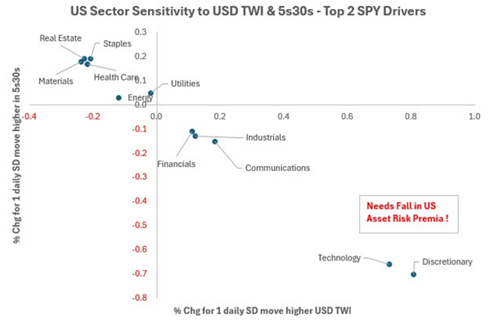

2. SPY sensitivity to the Dollar & 5s30s hitting extremes

Top Drivers: The S&P500 remains very well explained bymacro on our multi-month look back model, capturing the early Trump 2.0 era. Thetop 2 macro upside drivers? Stronger Dollar & flatter 5s30s i.e. proxies ofthe risk premia associated with the loss of US hegemonic power.

Multi-year extremes – can this persist? The sensitivity to the Dollar and5s30s is at multi-year highs. Tactically, bulls may question if this means concerns on the end of US exceptionalism have swung too far i.e. if China / UShave amicable talks these sensitivities would likely fade.

Sector implications: Any sign of trade war diffusion would aid Technology & Consumer Discretionary the most.

There are no major valuation gaps except in Energy: Macrovol has risen alongside the spot price weakness, keeping Qi model values broadly moving with spot. The top 20 stock winners / losers from Dollar weakness / steeper 5s30s (and vice versa) is shown below. Only 3 names are trading > 1 sigma below Qi model value (highlighted in green below).

3. What's priced? Global government bonds

10y US Treasury yields peaked near 4.60% on April 11th. That represented a 1.2sigma Fair Value Gap on Qi. That FVG has now effectively closed after thisweek's bond rally.

Duration bulls are betting off looking at Canadian govvies where the FVG has againnarrowed but yields still sit modestly high relative to the prevailing macro environment.

Theother standout is Japan - not in valuation terms, there are no FVGs of note. Morethat model confidence is high and JGBs are trading in line with model value,i.e. the market is behaving exactly as it should given macro conditions. Macromatters.

Disclaimer

This document is being sent only to investment professionals (as that term is defined in article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) OrdeRSq005 (“FPO”)) or to persons to whom it would otherwise be lawful to distribute it. Accordingly, persons who do not have professional experience in matters relating to investments should not rely on this document. The information contained herein is for general guidance and information only and is subject to amendment or correction. This document is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This document is provided for information purposes only, is intended for your use only, and does not constitute an invitation or offer to subscribe for or purchase any securities, any product or any service and neither this document nor anything contained herein shall form the basis of any contract or commitment whatsoever. This document does not constitute any recommendation regarding any securities, futures, derivatives or other investment products. The information contained herein is provided for informational and discussion purposes only and is not and, may not be relied on in any manner as accounting, legal, tax, investment, regulatory or other advice.

Information and opinions presented in this document have been obtained or derived from sources believed to be reliable, but Quant Insight Limited (Qi) makes no representation as to their accuracy or completeness or reliability and expressly disclaims any liability, including incidental or consequential damages arising from errors in this publication. No reliance may be placed for any purpose on the information and opinions contained in this document. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document by any of Qi, its employees or affiliates and no liability is accepted by such persons for the accuracy or completeness of any such information or opinions. Any data provided in this document indicating past performance is not a reliable indicator of future returns/performance. Nothing contained herein shall be relied upon as a promise or representation whether as to past or future performance.

This presentation is strictly confidential and may not be reproduced or redistributed in whole or in part nor may its contents be disclosed to any other person under any circumstances without the express permission of Quant Insight Limited.