1. The FX market is risk averse

2. The rates market is complacent

3. Bond vol complacency raising the ante for long duration equities

4. Momentum - buy the dip?

5. Chinese pivot? Equities, maybe. Bonds, not yet

6. Oil Stocks vs. Consumer discretionary in the US

1. The FX market is risk averse

Last week we flagged how several Yen crosses were too low and risk-reward favoured a bounce inAUDJPY, NZDJPY and EURJPY. All three have bounced but remain cheap on Qi. This week the machinehas turned bearish on the world's other safe haven currency, the Swiss Franc.

Swissy is uniformly rich to its G7 peers on Qi's models. And it's not just today's SNB decision. The SNB'saggressive 50bp rate cut helps; as does the sharp revision in their 2025 inflation forecast (from +0.6%to +0.3%). But Qi was saying the Swiss Franc was already rich to interest rate differentials even before today.

The other factor driving several CHF crosses are commodities. Copper & WTI are the top positivedrivers for the three biggest FVGs (AUDCF, NZDCHF & EURCHF) so the uptick after the Chinese policyannouncement have pushed Qi model value higher.

In terms of back-tests, AUDCHF has been the strongest signal - it's been in regime and this cheap tomodel 18x since 2009. The hit rate is 61% with a +0.7% average return. The correlation between spotand Qi FVG is strong too suggesting our Fair Value Gaps have done a good job of marking local highsand lows.If the FX market can catch some of the equity's market "risk on" vibe, there's more downside for theYen & Swiss Franc from here.

2. The rates market is complacent

The gunshot reaction to last month's US election was that a Trump Presidency would be inflationaryand therefore bond negative. A month later the script has flipped. Bonds have rallied on a newnarrative - that growth could suffer if tariffs spark a global trade war, or DOGE takes an axe to things.

Treasury yields have fallen, positioning has moved from short to long and bond volatility has collapsed.The MOVE index got close to the 2024 lows at 82.5. A break below that level hasn't been seen sinceearly 2022, i.e. the start of the Fed's hiking cycle.

Qi uses USD swaption volatility as a proxy for the size of the Fed's balance sheet, but investors can viewit as a broader liquidity measure guiding risk on / risk off sentiment. Which means the chart belowshowing the history of this factor in z-score terms offers a potential warning.US rate vol is now 1.5 standard deviations below trend. It rarely spends time below -2 sigma. An earlysign that interest rate volatility is falling into dangerously complacent territory.

3. Bond vol complacency raising the ante for long duration equities

We stated in our MacroHub publication this week that macro vol is currently not deemed to be aconcern into year end. CDX HY credit spreads have tightened further, VIX is hitting a 13-handle andequity rate vol as measured by the MOVE index is close to its 2024 lows.Yield curves across DM are back in positive territory i.e. term premium is making a comeback. Hence,the Central Banks will need to proceed carefully to mitigate the risks inflation expectations become unanchored.

We highlighted last week that the relative performance of longer duration stocks (biotech / nonprofitable tech etc.) vs. shorter duration stocks (e.g. oil drillers with visibility on near term cashflows)would be a good barometer to judge the market sentiment to rates. That basket pair has started tounderperform this week i.e. nerves are rising. It is becoming more noticeable that SPY has rallied <1% over the month.Another expression we think is undervalued relative to the risk of higher volatility ahead is mega captech over their non-profitable tech counterparts (pair at -1.75 sigma on Qi FVG). The latter facesmuch greater duration risk.

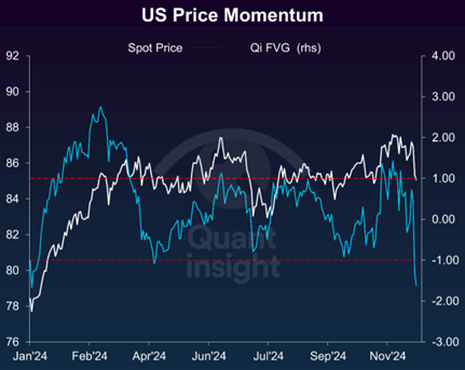

4. Momentum - buy the dip?

Since the election, the most popular HF longs have sharply underperformed the most popular shorts.In similar vein, the momentum style is seeing sharp underperformance. This follows a strongperformance in 2024 for this style factor. Seasonally, selling pressure on the winners after a strong year is to be expected. The momentum winners are tech-heavy.

Now last week small caps were the bigger under performers in US equities – our suspicion is that HFswho might have had to cover shorts on small caps post the election are probably done and arelooking to buy back into tech winners alongside year-end de-grossing into year end. YTD, the GS most short rolling basket has rallied 26%!As with the momentum style, the GS VIP basket is trading at a notable valuation discount to the GSmost short basket on Qi. The current narrative is maybe not so much about Nvidia as it is about the likes of now Zuckerberg and Bezos also seeking to work with Trump to shape deregulation. Within Tech, the SOXX remains the industry trading at the largest discount to macro warranted fair value (-1.65 sigma).

Buying Momentum when the spot price has dipped 1.6 sigma below the Qi model price (as seentoday), has proven to deliver positive returns two-thirds of the time, out of a sample of 15 trade events since 2009. See the two charts below.

5. Chinese pivot? Equities, maybe. Bonds, not yet.

Here we go again. Beijing has made positive noises about a meaningful shift in policy to support thedomestic economy. As in September, the key now is implementation risk - having made positive noises,will we now see practical steps to turn rhetoric into action?On Qi there are mixed messages. Macro-warranted model value for Chinese equities (FXI) lagged theSeptember rally but led the subsequent correction. Model value is showing tentative signs of stabilising(and maybe bouncing) but there isn't an unambiguous turn higher in macro momentum just yet.

And, in the meantime, this week's rally has overshot. Model confidence has fallen below our 65% threshold which precludes a bearish signal even if we hit 1 sigma rich (currently 0.9 std dev). This too needs watching as it could possibly indicate a regime shift is unfolding.

But potentially of more significance is the behaviour of the Chinese bond market. Qi’s Short Term model value is doing a better job of explaining price action right now and it continues to fall. In fact, macro momentum is accelerating lower.The only solace is that the market has front run this move suggesting yields have moved to price in a fair degree of the bad news already. But this is not an encouraging picture from a macro perspective –it suggests there is little sign from the bond market that the outlook for Chinese economic growth is improving.

6. Oil Stocks vs. Consumer discretionary in the US

US Oil stocks look cheap versus consumer discretionary stocks on the Qi model. The RV (using S5indices) is trading 1.8sigma cheap in favour of oil stocks -- close to a 5-year high. Momentum is also stretchedWe are at the 98th percentile in terms of valuation gap for the year and the there is a 75%correlation between the Qi fair value gap and the price of the RV, so our model has been a decent predictor over the last year.

The XLY Consumer ETF has had quite the run since the summer, going from 2sigma cheap to3.4sigma rich to the SPY -- also a 5-year highIf the recent monetary/Fx moves from China are an indicator/precursor of global easing then there may be a case for oil and commodities over consumption. The key drivers to make oil stocks outperform are stronger EU confidence and easier global financial conditions.