1. AII Sentiment & SPY Qi FVG hit 1yr lows, allowing for risk respite

2. EURCAD - who benefits in any Trump relief rally?

3. Shift in factor leadership for the Euro

1. AII Sentiment & SPY Qi FVG hit 1yr lows, allowing for risk respite

Markets continue to grapple on the question of the magnitude and breadth of tariffs. Arguably,the Dollar and long rates have already risen to partially price in uncertainty and a universal tariffscenario. Indeed, the AAII bulls less bears reading is now sitting at 1yr lows. And this is despite astring of consensus beating data. The implication is that a scenario of lighter / targeted / moregradual tariffs would garner the largest market reaction. Indeed, simply more clarity couldalleviate some of the risk premia.The S&P500 FVG also reached close to 1yr lows this week, mirroring the AAII sentiment reading(see the chart below). We see here that as market confidence has fallen / risen so has thedeviation of SPY spot to Qi model price fallen / risen. Ahead of Wednesday's CPI release, bothmeasures reflected the inclination that the larger price move would be for risk respite vs. furtherrisk pain. Clearly, when macro vol is high the uncertainty error as to whether the spot SPY pricewill converge back to the Qi model price is higher. That said, with positioning also light, the softerthan expected CPI release and Scott Bessent's testimony today, there is still a window for longrisky assets. The base case is surely that for both Trump & Bessent stockmarket confidencematters.

2. EURCAD - who benefits in any Trump relief rally?

Any suggestion of targeted or gradual tariffs has the potential to spark a relief rally in a number oftrades beaten up by the fears of a hard core “America First” approach. In FX, the Euro & CanadianDollar are amongst those in the firing line. So which is best placed to possibly benefit?While spot EURCAD has fallen around 1% in January, Qi model value has flat-lined. Real yielddifferentials have been a tailwind for macro-warranted model value, but wider European peripheralspreads have been an offsetting drag.

The net result is the cross sits 1.5 sigma (1.5%) cheap to aggregate macro conditions. The healthwarning is 51% model confidence means we're not in an official macro regime on Qi.Still, such gaps are rare. When including a 50% RSq constraint, it's only been seen 12x in the last 15years& back tests show a 75% hit rate. There's also been decent correlation between spot EURCAD & Qi'sFVG - our way of testing whether any mean reversion happens the "right" way.

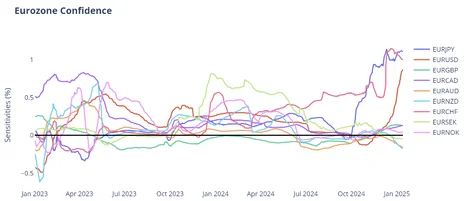

3. Shift in factor leadership for the Euro

It’s not just EURCAD where Qi model value has seen European peripheral spreads play a role. In fact,three Euro majors have seen a significant shift in factor leadership.Rate differentials are still the number 1 driver for EURUSD but peripheral spreads have become thesecond biggest factor in our model. In both EURJPY & EURCHF, sensitivity to EuroZone SovereignConfidence has risen to become the dominant driver of model value.

European peripheral spreads narrowed in the Trump rally but have started to leak wider once again.Events in France capture the dilemma. A compromise to pass a budget & avoid a no-confidence voteis clearly good for political stability. But the price it pays - watering down pension reform - meansdeficit concerns remain. Given the resurgence of bond vigilantes, fiscal laxity is a potential problem.The solace is both EURUSD & EURJPY both screen as over one standard deviation cheap - a degree ofbad news is priced in already. But FX investors need to keep an eye on European government bondspreads going forward - their reaction to domestic politics & Trump's policy agenda will have a majorbearing on how the single currency trades in the near term.

4. Long Materials for Offense & Long Staples for Defense

Both US Materials & European Basic Resources trade > 1 sigma below Qi model value. Is the markettoo bearish on the scope for a potential trade deal between the US and China? The CSI 300 is flat inreturn terms over the last 3mths. In contrast, European and US Materials are ~7% lower over thesame period. XME and EU Basic Resources have Qi FVGs of -1.89 sigma and -1.32 sigma, respectively.Below, we show the close relationship between the Qi FVG of EU Basic Resources and the spot price.Both are close to 1yr lows. The caveat is that the sector wants a stronger EURUSD and yields to topout. If treasuries are completing a bottoming process, so is likely this sector.

Similarly, since 2009 we see only 10 events where XME traded > 1.5 sigma below Qi model value.Going long the sector at this juncture yielded a 60% trade win rate with an average holding period of5-6 weeks.

What’s the cheapest risk-off hedge according to Qi? Consumer Staples. In particular, the equalweighted ETF RSPS – one of the few sectors with a positive sensitivity to VIX. RSPS is now trading1.65 sigma below Qi model value. See the chart below – the FVG is at 2yr lows.

5. European Consumer Goods - another European beneficiary from tariff gradualism

What else could benefit from any relief rally on any more gradual approach to tariffs? EU consumergoods screen as one of the cheapest areas on Qi. GS's basket of European consumer stocks sits 1sigma (2.8%) cheap to macro conditions.

That’s towards the cheap end of recent Valuation Gap ranges. It also scores well on back tests (82% hitrate, +2.7% average return); & in terms of Qi FVG doing a good job of capturing local turning points.